The Spouse Roth IRA Contribution is an essential financial tool for couples looking to enhance their retirement savings. This article delves deep into the nuances of Spouse Roth IRA contributions, shedding light on eligibility criteria, contribution limits, and strategic benefits. With the increasing importance of retirement planning, understanding how a Spouse Roth IRA can fit into your overall financial strategy is crucial for both partners to secure a comfortable future.

As the financial landscape evolves, so do the opportunities for couples to maximize their retirement savings. A Spouse Roth IRA allows one partner to contribute to the other’s retirement account, even if they don't have earned income. This unique feature can significantly impact your financial future, opening doors to tax-free growth and withdrawals in retirement.

In this article, we will explore the various aspects of Spouse Roth IRA contributions, including eligibility requirements, benefits, and strategies for effective implementation. By the end of this guide, you will have a thorough understanding of how to leverage this powerful tool to enhance your retirement planning.

Table of Contents

- What is a Spouse Roth IRA?

- Eligibility Requirements for Spouse Roth IRA Contributions

- Contribution Limits for Spouse Roth IRA

- Benefits of Contributing to a Spouse Roth IRA

- Strategies for Utilizing a Spouse Roth IRA Effectively

- Common Misconceptions about Spouse Roth IRA Contributions

- Tax Implications of Spouse Roth IRA Contributions

- Conclusion

What is a Spouse Roth IRA?

A Spouse Roth IRA is a type of retirement account that allows one spouse to contribute to the other spouse's Roth IRA, even if the contributing spouse does not have earned income. This arrangement is particularly beneficial for stay-at-home spouses or those working part-time. The contributions grow tax-free, and qualified withdrawals during retirement are also tax-free.

Key Features of Spouse Roth IRA

- Allows for tax-free growth and withdrawals.

- Contributions can be made regardless of earned income.

- Helps couples maximize their retirement savings.

Eligibility Requirements for Spouse Roth IRA Contributions

To qualify for Spouse Roth IRA contributions, several eligibility criteria must be met:

- Both spouses must file a joint tax return.

- The working spouse must have enough earned income to cover both contributions.

- Contributions are subject to income limits set by the IRS.

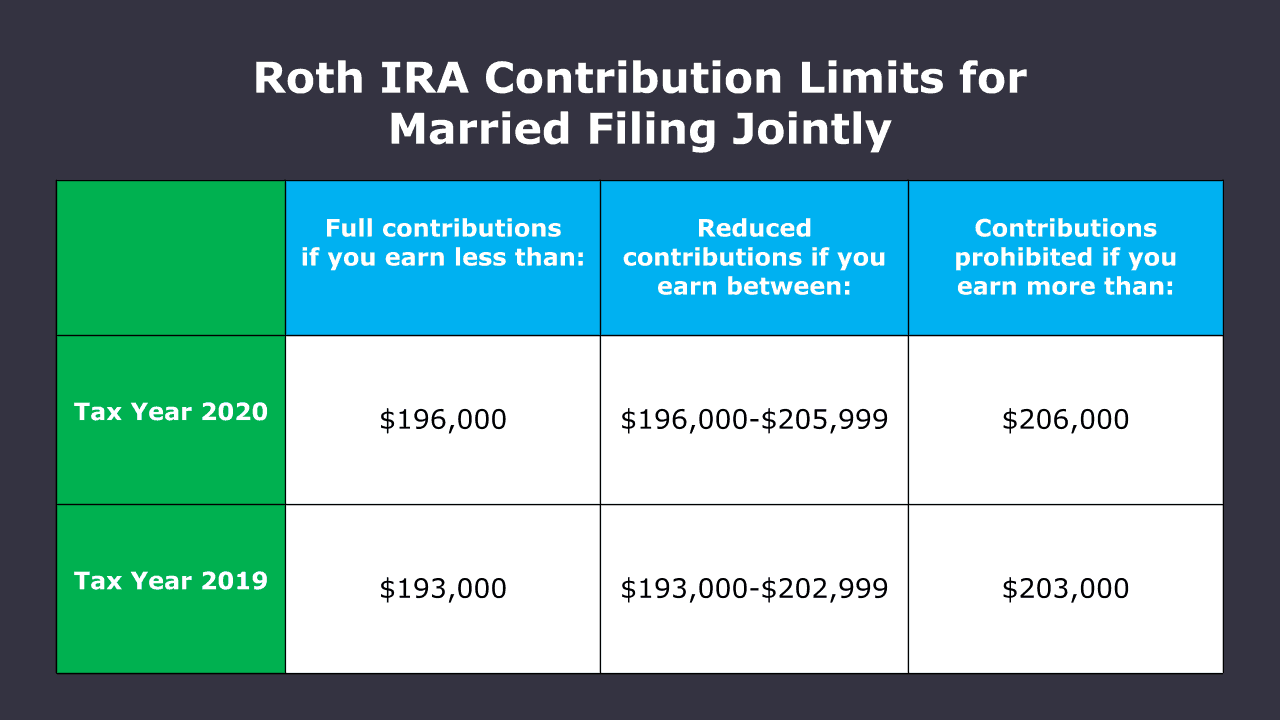

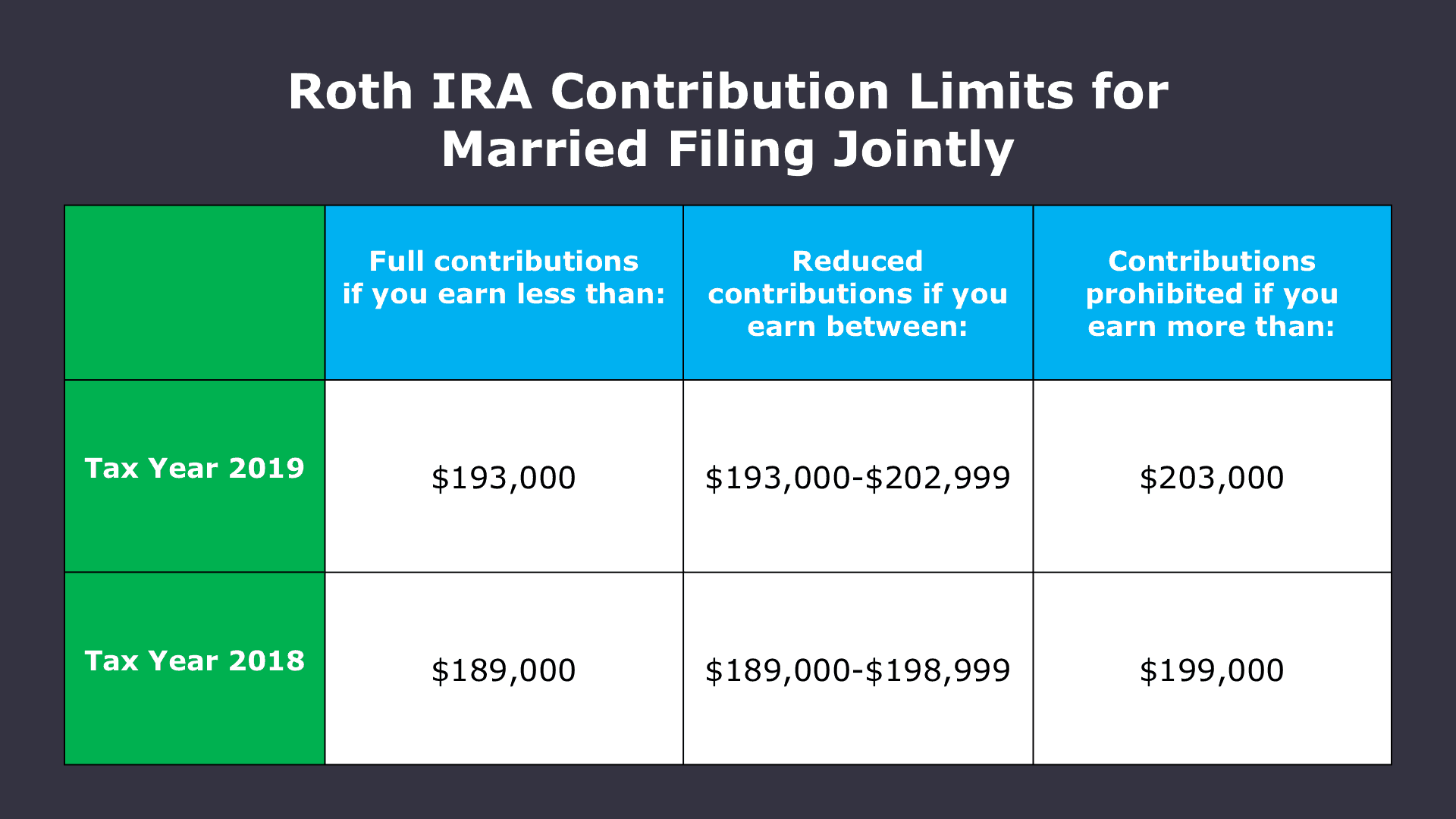

Contribution Limits for Spouse Roth IRA

The IRS sets annual contribution limits for Roth IRAs. As of 2023, the contribution limit for individuals is $6,500, or $7,500 for those aged 50 and older. For a Spouse Roth IRA, these limits are doubled if both spouses are eligible to contribute.

Example of Contribution Limits

| Age | Individual Contribution Limit | Couple Contribution Limit |

|---|---|---|

| Under 50 | $6,500 | $13,000 |

| 50 and Older | $7,500 | $15,000 |

Benefits of Contributing to a Spouse Roth IRA

There are several advantages to utilizing a Spouse Roth IRA, including:

- Tax-free growth and withdrawals.

- Increased retirement savings potential for couples.

- Flexibility in managing tax liabilities during retirement.

Strategies for Utilizing a Spouse Roth IRA Effectively

To maximize the benefits of a Spouse Roth IRA, consider the following strategies:

- Contribute up to the maximum limit each year.

- Diversify investment options within the Roth IRA.

- Plan for tax implications in retirement.

Common Misconceptions about Spouse Roth IRA Contributions

Many individuals have misconceptions when it comes to Spouse Roth IRA contributions. Here are a few common myths:

- Myth: Only the working spouse can make contributions.

- Myth: Roth IRAs are only for high earners.

- Myth: Contributions to a Spouse Roth IRA are taxable.

Tax Implications of Spouse Roth IRA Contributions

Understanding the tax implications of Spouse Roth IRA contributions is crucial. Contributions are made with after-tax dollars, and qualified withdrawals are tax-free. However, if you withdraw earnings before retirement age, you may face penalties.

Conclusion

In summary, the Spouse Roth IRA contribution is a powerful tool for couples looking to bolster their retirement savings. By understanding its benefits, eligibility criteria, and contribution limits, couples can strategically plan for a secure financial future. We encourage you to take action—consider consulting with a financial advisor to explore how a Spouse Roth IRA can fit into your retirement strategy.

Feel free to leave your thoughts in the comments below, share this article with others, and explore more content on our site for further financial insights!

Thank you for reading, and we look forward to seeing you again for more informative articles on retirement planning!

Ultimate Guide To Ozh.github.io Cookie Clicker: Tips, Tricks, And Strategies

Understanding Fidelity Index Funds: A Comprehensive Guide

Discovering Ginger Island West: A Hidden Gem Of Nature And Tranquility