Understanding the rate charged for borrowing when investing. A crucial component in maximizing investment returns.

The rate at which an investor borrows money to invest, often expressed as a percentage, is a fundamental aspect of investment strategies. This rate directly impacts the overall profitability of leveraged investments. For example, if an investor borrows at a 5% rate to purchase stocks, their returns must exceed that 5% to achieve a positive net gain. This rate is calculated and factored in various ways depending on individual investment products and policies. The margin rate is typically dependent on market conditions, the investor's creditworthiness, and the specific investment instrument involved.

A low margin rate can significantly enhance investment returns by reducing the financing costs associated with leveraging. This, in turn, allows for potentially greater gains. Conversely, a high margin rate can diminish returns, potentially leading to losses if the investment performance does not surpass the borrowing cost. Historical data shows that margin rates fluctuate based on economic conditions, with periods of high market volatility often correlating with higher rates. The financial institution providing the investment service typically sets and adjusts the rate.

Understanding this rate is essential for making informed investment decisions and managing investment risk effectively. The proper management of margin rates directly affects the overall financial outcomes of investments.

IB Margin Rate

Understanding the interest rate charged for borrowing to invest is critical for successful financial strategies. This rate directly influences the profitability of leveraged investments.

- Investment leverage

- Borrowing costs

- Interest rates

- Market conditions

- Profitability

- Risk assessment

- Investment instruments

- Financial institutions

IB margin rate, a key element in investment strategies, represents the borrowing cost. Market conditions significantly influence this rate. High rates during volatile periods increase the risk of investment losses if returns fall short. Conversely, low rates enhance returns if investment performance surpasses borrowing costs. Specific investment instruments (e.g., stocks) often have associated margin rates, and financial institutions set these rates based on factors like market conditions and an investor's creditworthiness. A comprehensive understanding of these aspects helps investors assess potential risks and maximize returns.

1. Investment Leverage

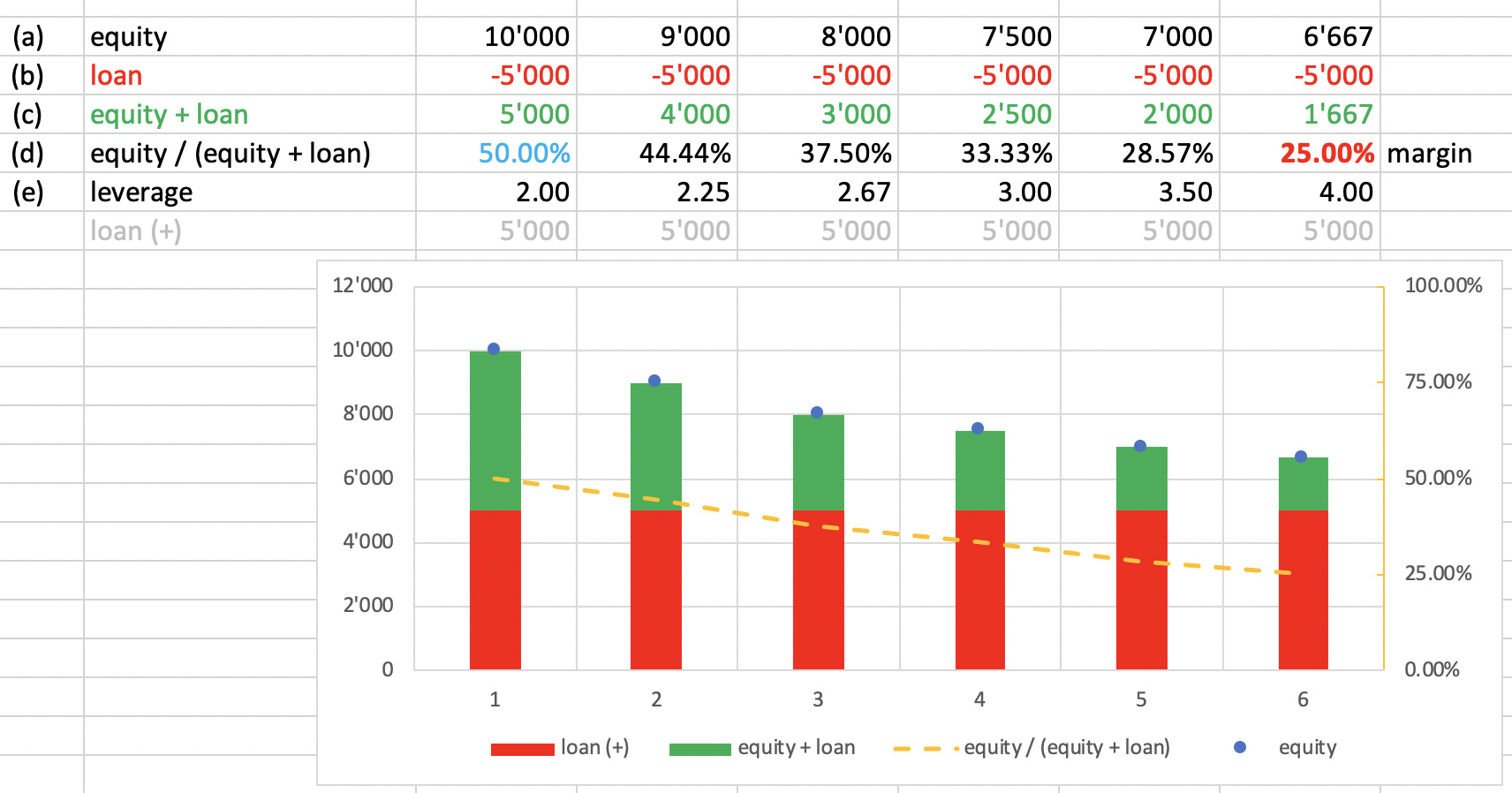

Investment leverage, a key component of many investment strategies, involves using borrowed funds to increase the potential return on investment. A fundamental aspect of this process is the associated borrowing cost. This cost is directly tied to the margin rate, a crucial determinant of profitability and risk. Higher margin rates translate into higher borrowing costs, reducing potential returns and amplifying potential losses if investment performance does not exceed the cost of borrowed capital. Conversely, lower margin rates make leverage more attractive, offering the prospect of magnified returns on successful investments but also increasing risk exposure to significant losses. For example, an investor utilizing a high margin rate to purchase stocks faces a substantial hurdle in achieving a positive return. A successful investment strategy needs to carefully consider the potential amplification of both gains and losses within this system.

The practical significance of understanding this connection is substantial. Investors need to assess the margin rate alongside projected investment returns to gauge the feasibility of leveraging strategies. A thorough analysis of historical data and current market conditions is vital in this process. Moreover, a clear understanding of how margin rates fluctuate with market volatility is essential for effective risk management. Investment decisions influenced solely by the potential for higher returns, without accounting for margin rates, can lead to significant financial losses. Careful consideration of the margin rate and potential return is crucial. Real-world examples demonstrate that ignoring this link can lead to costly mistakes in leveraging investments.

In summary, investment leverage and margin rate are inextricably linked. Investors must understand the interplay between these variables to make informed decisions, mitigating potential risks and maximizing potential gains. By incorporating a thorough analysis of margin rates into investment strategies, investors can enhance the probability of success in leveraged ventures. Ultimately, a prudent approach emphasizes calculated risk-taking while recognizing the importance of the margin rate in investment outcomes.

2. Borrowing Costs

Borrowing costs represent the expenses incurred when obtaining funds through loans or lines of credit. In the context of investment, borrowing costs are a direct component of margin rates. Margin rates fundamentally determine the price of borrowed capital, thereby shaping the overall cost of investment. A higher margin rate translates directly to higher borrowing costs, impacting the profitability of leveraged investments. Conversely, lower margin rates result in reduced borrowing costs, potentially increasing the attractiveness of leveraging strategies. This correlation highlights the critical importance of understanding borrowing costs as an integral aspect of margin rates in investment decisions.

The impact of borrowing costs is substantial. For instance, a high margin rate may render a leveraged investment unprofitable even if the underlying investment performs well. If the returns on the investment fail to exceed the borrowing costs associated with the margin rate, the investor experiences a net loss. Conversely, a favorable margin rateone that keeps borrowing costs lowenhances the likelihood of achieving positive returns in leveraged investments. Thus, the relationship between borrowing costs and margin rates directly influences the risk-reward profile of investment strategies. A rigorous analysis of these costs is essential for effective risk management, as the potential for magnified losses is inherent in leveraging strategies. Historically, periods of high market volatility often correlate with higher margin rates, resulting in increased borrowing costs and heightened investment risk.

In conclusion, borrowing costs are intrinsically linked to margin rates. Understanding this connection is crucial for informed investment decisions. Investors should meticulously analyze borrowing costs alongside anticipated returns to evaluate the feasibility of employing leveraged strategies. By acknowledging the role of borrowing costs as a critical factor within margin rates, investors can effectively manage risk and enhance the potential for positive investment outcomes. Failure to account for these costs can lead to substantial financial losses, reinforcing the importance of careful planning and due diligence.

3. Interest Rates

Interest rates play a pivotal role in determining margin rates. The relationship is direct and significant, influencing the cost of borrowing capital for investment purposes. Understanding this connection is essential for assessing the viability of leveraged investment strategies.

- Impact on Margin Rates

Interest rates and margin rates are intrinsically linked. Margin rates are often set at a premium above prevailing interest rates, reflecting the added risk inherent in margin lending. Changes in prevailing interest rates directly impact the cost of borrowing and consequently influence margin rates. For instance, if short-term interest rates rise, margin rates typically increase as well, making leveraging more expensive. Conversely, a decline in interest rates typically leads to lower margin rates.

- Market Volatility and Fluctuations

Market fluctuations often correlate with changes in both interest rates and margin rates. During periods of economic uncertainty or heightened market volatility, borrowing costs tend to rise, influencing the margin rate upward. This reaction is often a defensive measure by financial institutions, reflecting their assessment of increased risk. In contrast, periods of stability and confidence in the markets might see both interest rates and margin rates decrease, making leveraged investments potentially more accessible.

- Bank Lending Practices

Central bank policies significantly influence both interest rates and margin rates. Central banks' adjustments to monetary policy directly affect short-term interest rates, which, in turn, frequently dictate the base levels for various margin rates. Banks then often factor in their own risk assessments when setting the margin rate for specific instruments and investors, influencing the final margin rates offered.

- Investor Behavior and Market Perception

The perception of market risk also influences margin rates, potentially leading to a correlation independent of interest rate changes. Investors' overall risk tolerance and market sentiment can impact margin rates. For example, if investors perceive a greater risk in the market, institutions may react by increasing margin rates to mitigate risk exposure, even if interest rates remain stable.

In conclusion, the relationship between interest rates and margin rates is multifaceted. Understanding how interest rate fluctuations impact margin rates is crucial for investors navigating the complexities of leveraged investment. The interwoven nature of these factors requires a thorough analysis of prevailing interest rates, market sentiment, and bank lending practices to accurately assess and mitigate the risks inherent in margin-based investment strategies.

4. Market Conditions

Market conditions exert a significant influence on margin rates. This influence is not arbitrary; it reflects the inherent risk associated with borrowing to invest. During periods of economic uncertainty or heightened market volatility, the perceived risk of investors defaulting on their margin loans increases. As a result, financial institutions typically raise margin rates to mitigate this elevated risk. Conversely, in stable markets, the risk is lower, and margin rates often decrease. This dynamic underscores a crucial link between market sentiment and the cost of borrowing for investment.

Consider the impact of a sudden market downturn. If stock prices plummet, investors who have borrowed heavily to purchase these stocks face a substantial risk of not being able to cover their margin calls. Financial institutions, recognizing this increased risk, respond by raising margin rates. Higher rates make leveraging less attractive, potentially curbing further declines in the market. This reactive adjustment to market conditions demonstrates how margin rates are not static but actively adjust to reflect changing market dynamics. Conversely, during periods of sustained market growth and investor confidence, margin rates typically fall, as the perceived risk decreases. These fluctuations directly impact the investment decisions of individuals and institutions, influencing their choices concerning leveraged strategies.

Understanding the interplay between market conditions and margin rates is crucial for effective risk management. Investors need to factor in these fluctuations when evaluating investment opportunities. An investment strategy that ignores this correlation risks significant financial losses, particularly in volatile markets. A thorough understanding of market conditions, coupled with a realistic assessment of personal risk tolerance and the impact of margin rates, is essential for navigating the complexities of leveraged investment. Ultimately, the dynamic interplay between market conditions and margin rates represents a significant element in the investment landscape, requiring proactive monitoring and strategic responses to effectively manage risk.

5. Profitability

Profitability, in the context of investment strategies utilizing borrowed capital, is intricately linked to margin rates. Margin rates directly affect the cost of borrowing, which in turn impacts the potential for positive returns. A thorough understanding of this connection is essential for optimizing investment decisions and mitigating potential losses.

- Return on Investment (ROI) Calculation

Profitability hinges on the relationship between investment returns and borrowing costs. A high margin rate directly increases the cost of borrowed capital, reducing the net return. If investment returns do not surpass the margin rate, profitability suffers. For instance, if an investment generates 8% in returns while the margin rate is 10%, the investor incurs a net loss. Conversely, low margin rates allow for a larger potential ROI, as a greater proportion of investment gains accrue to the investor.

- Leverage and Magnified Results

Leverage amplifies both potential gains and losses. A lower margin rate makes leveraged investment strategies more attractive, as the cost of borrowing is reduced, thus increasing the potential for amplified gains. However, the reverse holds true: a high margin rate substantially reduces potential profits and significantly increases the risk of losses in a leveraged investment scenario. This underscores the vital role of margin rates in determining overall profitability.

- Margin Calls and Potential Losses

High margin rates can trigger margin calls, necessitating additional capital to maintain investment positions. Failing to meet a margin call can lead to significant losses, highlighting the crucial connection between margin rates and overall profitability. In volatile markets, high margin rates intensify this risk, making leveraged investment strategies significantly less profitable and potentially ruinous. Conversely, low margin rates lessen the probability of a margin call, providing more stability and a higher likelihood of positive returns.

- Historical Performance and Forecasting

Analyzing historical data concerning margin rates and profitability can reveal valuable trends. Patterns and correlations between margin rates and investment performance can provide crucial insights for forecasting future profitability. However, caution is paramount, as market conditions are dynamic and past performance is not necessarily indicative of future results. Historical analysis must be combined with a thorough understanding of the current market context and the investment instrument.

In summary, profitability in leveraged investment strategies is fundamentally linked to margin rates. Lower rates facilitate greater potential for positive returns, while high rates increase the risk of losses and diminish profitability. Investors must thoroughly consider the interplay between margin rates, market conditions, and potential returns when evaluating the viability and profitability of their investment strategies. A prudent approach that accounts for these factors is crucial for maximizing returns and minimizing risk.

6. Risk Assessment

Risk assessment is inextricably linked to margin rates. A critical component of any investment strategy involving borrowed capital, risk assessment directly influences the determination of margin rates. Higher perceived risk often results in higher margin rates, reflecting the increased likelihood of default or difficulty meeting margin calls. Conversely, lower perceived risk typically leads to lower margin rates, making leveraged investment strategies potentially more attractive. The relationship hinges on the financial institution's evaluation of the investor's ability to repay borrowed funds, taking into account factors such as creditworthiness, market conditions, and the nature of the investment itself.

The importance of risk assessment as a determinant of margin rates stems from the inherent amplification of both potential gains and losses in leveraged investments. A thorough risk assessment considers various factors, including the investor's financial history, the current market environment, and the specific investment instrument. For example, a volatile market with a high degree of uncertainty will likely lead to higher margin rates, while a stable market may permit lower rates. The degree of leverage used also impacts the assessmenthigher leverage implies greater risk and, consequently, potentially higher margin rates. A well-executed risk assessment allows for more precise pricing of the risk embedded in the margin loan, enhancing the efficiency of capital allocation. Real-world examples abound; institutions raising margin rates during economic downturns or for risky investment instruments underscores the direct connection between risk assessment and margin rates.

In conclusion, risk assessment is a fundamental element in determining margin rates. Understanding this connection is crucial for investors to make informed decisions and mitigate potential losses. A comprehensive risk assessment process, factoring in market volatility, the investor's financial capacity, and the characteristics of the investment, allows for a more accurate evaluation of the associated risks. This precision is vital in managing the inherent amplification of both gains and losses in leveraged investments. This proactive approach to risk assessment enables investors to strategically leverage capital while minimizing the financial jeopardy associated with margin-based investment strategies.

7. Investment Instruments

The type of investment instrument significantly influences the margin rate applied. Different assets carry varying degrees of risk, directly affecting the borrowing cost. Understanding this relationship is crucial for investors to make informed decisions about leveraging investments.

- Stocks

Margin rates on stocks often fluctuate more dynamically than those on other assets. Market volatility and the inherent risk associated with stock price fluctuations directly impact the margin rate. High trading volumes, short-term price swings, and the potential for rapid stock price declines all contribute to a higher perceived risk, leading to higher margin rates. Historical data reveals a strong correlation between market downturns and increased margin rates on stocks. Lower margin rates might be applied during periods of strong market stability and steady stock performance.

- Bonds

Margin rates on bonds, generally, are lower than those on stocks. Bonds are considered less risky investments due to their fixed income nature, meaning the issuer's obligation to pay a set amount of interest and principal. This lower risk perception translates to a lower margin rate. However, the creditworthiness of the bond issuer still influences the rate; higher-risk bonds issued by companies with questionable credit histories will usually have higher margin rates. The length of time until maturity also factors in, with longer-term bonds carrying some additional risk.

- Commodities

Margin rates on commodities can vary considerably depending on the specific commodity. Commodities like gold, which are considered relatively stable, often have lower margin rates compared to more volatile commodities. Factors such as supply and demand dynamics and global market trends influence the perceived risk and subsequently the margin rate applied to commodity investments. The high leverage potential associated with commodities also plays a role, influencing the institutions' risk assessment and leading to higher margin rates compared to more established investments.

- Real Estate

Margin rates on real estate investments, including mortgages or real estate investment trusts (REITs), are often lower than those on highly volatile assets. The relative stability of real estate markets, even during economic downturns, contributes to this lower margin rate. However, factors like location, property type, and market conditions can impact the perceived risk and, therefore, the applicable margin rate. The complexity involved in real estate transactions also necessitates a closer assessment by financial institutions to determine the precise risk assessment and subsequently the margin rates.

In essence, the choice of investment instrument fundamentally impacts the margin rate applied. Understanding this interplay allows investors to make more informed decisions about leveraging strategies, considering both potential returns and the associated costs of borrowing. The diverse characteristics of various investment instruments necessitate a tailored risk assessment by financial institutions, leading to differentiated margin rates. Careful consideration of each instrument's risk profile, coupled with prevailing market conditions, is imperative for maximizing potential returns while minimizing risk.

8. Financial Institutions

Financial institutions play a critical role in establishing and adjusting margin rates. Their decisions regarding margin rates are not arbitrary but reflect a complex assessment of various factors. These factors include prevailing market conditions, the level of risk associated with different investment instruments, and the creditworthiness of individual investors. The relationship is fundamental; institutions set margin rates to manage their own risk exposure while considering market dynamics and investor behavior. A rise or fall in market volatility will often correspond with changes to these margin rates.

The importance of financial institutions in establishing margin rates cannot be overstated. They act as intermediaries in the investment process, balancing the needs of investors seeking leverage with their own risk management objectives. For instance, during periods of heightened market uncertainty, financial institutions might increase margin rates to mitigate potential losses from investor defaults. This response to perceived risk serves to protect the institution's capital and maintain stability within the financial system. Conversely, during periods of market optimism, institutions may lower margin rates to encourage investment and foster economic activity. These adjustments demonstrate a dynamic and reactive relationship between financial institutions and the investment market. Examples include increased margin rates during the 2008 financial crisis, designed to curtail excessive risk-taking, and subsequent reductions as market stability improved.

Financial institutions' role in setting margin rates is vital for the smooth functioning of the investment market. Their ability to adjust margin rates based on a complex evaluation of market factors is crucial for managing risk and maintaining stability. Understanding this crucial relationship allows investors to make more informed decisions by anticipating how market changes will affect borrowing costs. This understanding is essential to effectively manage the risks associated with leveraged investments. This relationship demonstrates the crucial balance between fostering economic activity and ensuring the financial well-being of the institutions themselves.

Frequently Asked Questions about IB Margin Rates

This section addresses common queries regarding IB margin rates, providing clarity on this critical component of leveraged investment strategies. Precise understanding of these rates is essential for informed investment decisions.

Question 1: What is an IB margin rate, and how does it work?

An IB margin rate is the interest rate charged by an investment brokerage (IB) when an investor borrows money to invest. This rate is calculated based on several factors, including the current market conditions, the investor's creditworthiness, and the specific investment instrument being leveraged. The IB sets the margin rate, which directly impacts the cost of borrowing funds for investment purposes. The higher the rate, the greater the cost of borrowing and the potential reduction in profitability.

Question 2: How do market conditions affect IB margin rates?

Market conditions play a significant role in determining IB margin rates. During periods of heightened market volatility or economic uncertainty, the perceived risk of investor defaults increases. Consequently, institutions typically increase margin rates to mitigate this risk. Conversely, in stable markets, margin rates tend to decrease, reflecting the lower perceived risk. This dynamic connection underscores the importance of market awareness for investors considering leveraged strategies.

Question 3: What are the factors influencing an IB's decision on margin rates?

Several factors contribute to an IB's determination of margin rates. These include the prevailing interest rates, the specific investment instrument being leveraged, the investor's creditworthiness, and the institution's assessment of the overall market risk. All these factors are carefully considered to strike a balance between investor opportunities and the institution's risk management practices.

Question 4: How does the choice of investment instrument affect the IB margin rate?

Different investment instruments carry varying degrees of risk, directly impacting the applicable margin rate. Assets like stocks, with their price volatility, typically have higher margin rates compared to more stable investments like bonds. The perceived risk associated with each instrument is a key factor in determining the margin rate charged by the institution.

Question 5: What are the potential consequences of not understanding IB margin rates?

Failing to understand IB margin rates can lead to significant financial repercussions. High margin rates can diminish potential profits and may trigger margin calls, necessitating additional funds to maintain investment positions. Unforeseen increases in margin rates can result in substantial losses if investment returns do not exceed the cost of borrowing. Therefore, a thorough understanding of margin rates is crucial for effectively managing risk in leveraged investment strategies.

Understanding IB margin rates is essential for investors navigating leveraged investment strategies. A careful assessment of these rates, coupled with a thorough understanding of market conditions and personal risk tolerance, is crucial for informed and successful investment decisions. The information presented here serves as a starting point for further research and consultation with financial professionals.

Transition to next section: Further exploration into investment strategies and risk management practices.

Conclusion

IB margin rates represent a critical component of leveraged investment strategies. This analysis highlights the multifaceted nature of this rate, exploring its dependence on market conditions, investment instruments, and the financial institution's risk assessment. The interplay between interest rates, market volatility, and the investor's creditworthiness directly influences the cost of borrowing capital. Understanding the dynamic relationship between margin rates and investment instrument risk is crucial for effective risk management. Moreover, the crucial role of financial institutions in establishing and adjusting these rates emphasizes their responsibility in balancing market opportunities with risk mitigation. A thorough grasp of these factors is essential for informed decisions regarding leveraging investments, enabling a more calculated and potentially more profitable approach to investment strategies.

In conclusion, the IB margin rate is not a static figure but a dynamic variable responsive to a complex interplay of economic forces and financial institution practices. Investors should rigorously assess these factors and their potential impact on investment outcomes when considering leveraged strategies. The future of investment markets demands a continuous and insightful approach to understanding these rate fluctuations and incorporating that knowledge into personalized investment approaches. Only through this proactive engagement can investors effectively navigate the complexities of the financial landscape and realize potential benefits while managing associated risks.

Klip Next Dividend Date - When To Expect It

Aflac Dental Coverage Review: 2023 Expert Analysis & Summary

William E. Oberndorf: Key Insights & Details