Determining the appropriate level of flood insurance protection is crucial for safeguarding one's property and financial well-being. A comprehensive understanding of flood risk and available insurance options is paramount.

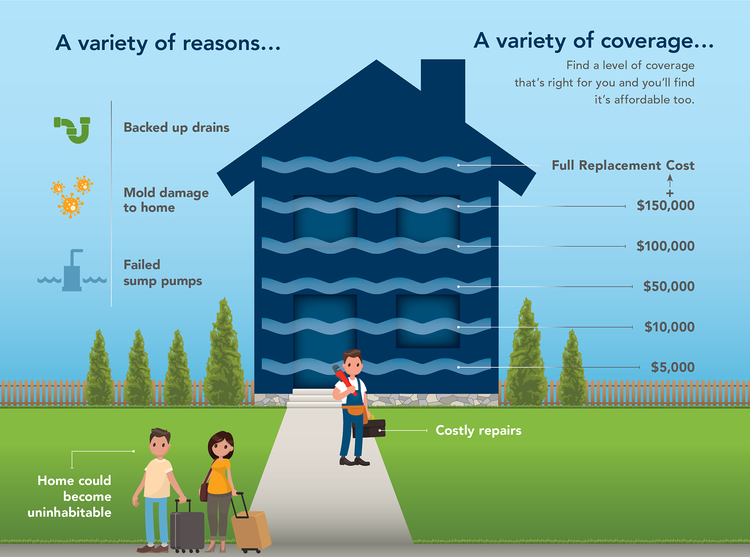

Determining the adequate level of water backup protection hinges on several factors. These include the property's vulnerability to flooding, the potential severity of flood events in the area, and the financial capacity to absorb potential losses. Assessing the likelihood of flooding, from localized storms to more widespread events, informs the appropriate coverage amount. For example, a property situated in a flood plain with a documented history of significant flooding necessitates higher levels of coverage than a property situated in a less prone area. The extent of the property's potential damage, whether to the structure, contents, or both, is also a critical factor in determining the optimal coverage amount.

Adequate water backup insurance safeguards against substantial financial losses stemming from flooding. Protecting possessions and potentially rebuilding a damaged property or making essential repairs are paramount. The historical context of flooding in the area provides valuable data for assessing future risks and selecting the appropriate insurance package. Understanding past flood events allows for a more informed and responsible approach to risk management and financial preparedness. In essence, the correct level of protection involves a careful balancing act between potential risks and necessary safeguards. Comprehensive analysis and a cautious approach are essential to achieving this balance.

How Much Water Backup Coverage Do I Need?

Determining the appropriate water backup coverage is crucial for safeguarding financial interests and property. Understanding the essential factors involved ensures sufficient protection against potential losses. This assessment depends on multiple key elements.

- Property Value

- Flood Risk

- Contents Coverage

- Policy Limits

- Coverage Options

- Local Regulations

- Financial Capacity

Property value directly influences the necessary coverage amount. Higher-value properties require greater flood insurance protection. Flood risk assessment, considering geographic location and historical data, dictates coverage limits. Coverage for contents, beyond the structure, is crucial. Policy limits and available coverage options influence the total insurance needed. Local regulations might dictate minimum coverage amounts. Financial capacity to absorb potential losses should also be a factor in determining appropriate insurance. These factors combine to create a nuanced approach to securing appropriate protection from water damage.

1. Property Value

Property value directly correlates with the amount of water backup coverage required. A higher property value necessitates a higher insurance coverage amount to adequately compensate for potential losses. This is because the financial impact of a flood event on a high-value property is proportionally greater. For instance, a home valued at $500,000 will likely require a substantially larger insurance policy than a home valued at $150,000, considering the same level of flood risk. This fundamental principle underscores the importance of accurately assessing property value for appropriate flood insurance coverage. The amount of coverage required also depends on the level of personal belongings within the property, further increasing the value of the property and the required insurance.

The relationship between property value and coverage isn't static. Factors like location, construction quality, and contents influence the overall value at risk. A high-value home built with flood-resistant materials in a low-risk flood zone might require less coverage compared to a similarly priced home in a high-risk area with less robust construction. Furthermore, the extent of personal belongings within the home significantly impacts the need for additional coverage. The total combined value of the home and its contents form a basis for the required insurance coverage. Accurate appraisals of both the structure and contents are essential to obtaining the correct coverage amount and avoiding significant financial vulnerability in the event of a water backup.

Understanding the direct link between property value and required water backup coverage is essential for financial preparedness. A thorough assessment of property value, considering all relevant factors, is crucial for determining the right level of coverage. This approach avoids both underinsurance, which leaves one exposed to significant financial losses, and overinsurance, which incurs unnecessary premium costs. Accurate valuation of assets and a prudent evaluation of associated risks are pivotal for obtaining suitable flood insurance and mitigating the risks of a water backup event.

2. Flood Risk

Flood risk is a primary determinant in calculating the appropriate level of water backup coverage. Areas with a higher historical frequency and severity of flooding necessitate more comprehensive insurance. Floodplains, proximity to rivers or streams, and past flood events are critical data points. Elevated flood risk necessitates increased coverage to address potential damage and rebuild costs. This principle directly influences the financial preparedness for potential losses associated with water damage. A meticulous assessment of flood risk, including historical data, elevation, and geographic features, informs a tailored insurance strategy. Real-life examples demonstrate that homes in flood-prone areas experience significantly greater flood damage compared to those situated in areas with lower flood risk.

Assessing flood risk involves a multifaceted approach. Local flood maps, which visually delineate flood zones, provide crucial information. These maps show the extent and potential depth of floodwaters, offering a direct correlation between geographical location and flood risk. Furthermore, historical flood records, including details of previous events, identify recurring flood patterns and their potential severity. Statistical analyses of these records can predict the likelihood of future flooding, allowing for more precise risk assessment and coverage calculations. Moreover, understanding regional climate patterns, including rainfall intensity and duration, significantly influences the likelihood of flooding in various areas. The interplay between these factors establishes a clearer picture of flood vulnerability, guiding appropriate insurance selection. This detailed understanding of flood risk is directly applicable when evaluating the appropriate level of water backup coverage to secure financial protection against potential losses.

In conclusion, the accurate assessment of flood risk is essential for establishing appropriate water backup coverage. A thorough evaluation of historical data, geographic location, and local climate patterns yields a clearer understanding of potential flood vulnerability. This crucial component of risk assessment directly guides insurance decisions, ensuring financial protection in the event of a flood. Understanding flood risk and its corresponding financial implications leads to a proactive approach to safeguarding assets and mitigating financial exposure associated with water damage.

3. Contents Coverage

Determining the appropriate level of water backup coverage necessitates a comprehensive understanding of contents coverage. The value of personal belongings significantly influences the required insurance amount. Failure to adequately insure contents leaves individuals vulnerable to substantial financial losses in the event of water damage. This section explores key facets of contents coverage and their importance in total water backup insurance.

- Valuation of Personal Possessions

Accurate assessment of personal belongings is paramount. This involves meticulously listing and valuing items, considering their current market price or replacement cost. Digital records of possessions (photos, inventories, receipts) are crucial for claims. Factors such as age, condition, and uniqueness of items all contribute to the overall valuation. A high-value collection, such as artwork or antiques, may necessitate specific appraisal procedures. This thorough inventory ensures accurate claims processing and compensation.

- Coverage Limits and Deductibles

Understanding coverage limits and deductibles is essential. Coverage limits determine the maximum amount the insurance provider will compensate for water damage to personal belongings. Deductibles represent the amount an individual must pay out-of-pocket before insurance coverage applies. By carefully comparing policy offerings and understanding the trade-offs between limits and deductibles, one can tailor insurance to personal financial circumstances and the perceived level of risk.

- Specific Item Coverage Considerations

Certain items may require special attention. Valuables, such as jewelry or electronic equipment, often have a higher risk of loss and thus may necessitate specialized coverage. Specific insurance provisions may be needed for sentimental items or collectibles with unique or historical value. These items are often independently appraised to ensure appropriate insurance and a proper compensation structure in case of loss.

- Replacement Cost vs. Actual Cash Value

Understanding the differences between replacement cost and actual cash value is crucial. Replacement cost coverage compensates for the cost of replacing damaged items at current market prices, while actual cash value accounts for depreciation. The choice between these options depends on individual preferences and financial considerations. This understanding of valuation methodologies ensures clarity and accuracy when assessing the required coverage for personal belongings in the face of water damage.

In summary, contents coverage is an integral part of adequate water backup insurance. Comprehensive valuation of personal belongings, awareness of coverage limits, and consideration of specific item requirements are critical steps in securing sufficient protection. Understanding the nuances of replacement cost versus actual cash value further enhances informed insurance decisions. The combination of these factors ensures accurate financial preparedness for the potential financial burdens associated with water damage and the loss of personal possessions.

4. Policy Limits

Policy limits are a critical aspect of determining the appropriate level of water backup coverage. These limits directly impact the maximum amount an insurance policy will pay out in the event of a covered loss. Understanding these limits is essential for ensuring sufficient protection against potential financial consequences. The interplay between policy limits, potential damages, and the overall financial risk profile guides decisions about adequate coverage.

- Coverage Amount Determination

Policy limits establish the upper bound for reimbursement. The specific coverage amount needed depends on the calculated value of the property and its contents, potential damage scenarios, and the individual's financial capacity. A detailed assessment of these factors directly informs the appropriate policy limit to ensure financial protection. Failure to accurately reflect these factors can result in insufficient coverage, potentially leaving an individual vulnerable to significant financial hardship in the event of a covered loss.

- Relationship with Potential Damage

Policy limits must be realistically aligned with potential damage estimates. Estimating the potential loss, from damage to the structure to the contents, requires careful consideration. Analyzing past flood events in the area, coupled with assessments of the property's vulnerability, helps quantify the potential damage. A policy limit too low in relation to potential damage may fail to adequately address financial needs. Conversely, a limit excessively high compared to the anticipated damage could lead to unnecessary insurance premiums.

- Impact on Rebuilding or Repair Costs

Policy limits directly influence the ability to cover rebuilding or repair costs. An adequate policy limit is essential to ensure comprehensive financial coverage for potential structural or non-structural damages. Understanding the potential costs associated with restoration or reconstruction is critical for setting appropriate policy limits. Realistic estimates of reconstruction costs, informed by local contractors and market rates, guide insurance decisions. This, in turn, ensures financial resources to rebuild or repair the property to its pre-loss condition.

- Financial Capacity and Risk Tolerance

Considerations of personal finances and risk tolerance are crucial in selecting appropriate policy limits. Understanding the financial capacity to absorb potential losses is paramount when choosing policy limits. The decision-making process should account for the potential financial implications. This includes a realistic assessment of personal savings, existing insurance coverage, and the ability to manage potential losses beyond the policy limits.

Ultimately, appropriate policy limits are essential for ensuring adequate water backup coverage. Understanding the relationship between policy limits, potential damage, and individual financial capacity guides a sound approach to insurance. Careful consideration of these factors directly translates to an informed decision, ultimately mitigating financial risk and securing financial protection against water damage.

5. Coverage Options

Understanding available coverage options is fundamental to determining the appropriate level of water backup insurance. Different policy structures offer varying degrees of protection, influencing the amount of coverage required. These options encompass a range of protections tailored to specific needs and risks.

- Structure Coverage

This component addresses damage to the physical building itself. Different levels of structure coverage cater to varying needs. A policy covering only the dwelling's structure might be suitable for a property with robust construction in a low-risk flood zone. However, for properties in high-risk areas, comprehensive structure coverage, including exterior walls, roof, and foundation, is essential. The amount of structure coverage directly relates to the estimated rebuilding cost of the affected structures after a flood.

- Contents Coverage

This component encompasses coverage for personal belongings within the structure. Options exist for covering furniture, appliances, clothing, and other possessions. The extent of contents coverage is vital and depends on the value of the belongings and the potential for loss. Policies vary in whether they offer replacement cost or actual cash value for damaged items, influencing the financial compensation in case of damage.

- Additional Living Expenses

This component covers living expenses during a period when a property is uninhabitable due to water damage. It provides funds to cover lodging, meals, and other essential expenses while repairs are underway. A higher level of additional living expenses coverage might be necessary for longer restoration periods. The option to cover additional living expenses can significantly mitigate the financial strain experienced by homeowners during a water damage incident.

- Flood-Specific Add-ons

Flood-specific coverage, beyond standard policies, is often required in high-risk areas. Flooding can cause extensive damage, often beyond the scope of standard home insurance. These add-ons provide coverage tailored to the particular risks associated with flooding. The amount of coverage for flood-specific issues like damage to sewer and water systems should be substantial for properties prone to such events. This specific coverage allows for comprehensive financial recovery in the face of potentially devastating flooding events.

The interplay of these coverage options directly shapes the ultimate insurance premium and the financial protection afforded. Choosing the correct blend of structural, contents, and additional living expense options allows one to tailor the insurance to a personal risk tolerance and financial capacity. Considering a comprehensive flood-specific add-on ensures a layered approach to financial protection in a high-risk area.

6. Local Regulations

Local regulations significantly influence the amount of water backup coverage required. These regulations often mandate minimum levels of insurance coverage, especially in high-risk flood zones. Compliance with local ordinances is essential to protect property and financial interests. Failure to meet mandated coverage levels can lead to penalties or even denial of building permits or other crucial approvals. This direct link between regulations and insurance dictates a critical component of assessing overall water backup protection.

Specific regulations vary geographically. Some jurisdictions require higher coverage for properties situated in floodplains or areas with a history of significant flooding. These regulations reflect a community's risk assessment and prioritize the financial security of residents. For example, a municipality experiencing frequent flooding might mandate increased flood insurance limits for all properties within designated flood zones. Conversely, areas with a lower risk of flooding might have less stringent insurance requirements. Understanding these regional differences is paramount for accurate coverage estimations. Moreover, building codes and zoning regulations can indirectly affect coverage needs. Flood-resistant building practices, mandated by local codes, can influence the perceived risk and, consequently, the amount of insurance deemed sufficient. Compliance with local building codes and regulations, including those related to flood resilience, often dictates the minimum level of insurance considered acceptable.

A thorough understanding of local regulations regarding water backup coverage is crucial for financial preparedness. Ignorance of mandated minimums can result in inadequate protection against potential water damage. Understanding these rules and regulations empowers individuals to make informed choices about insurance, ensuring adequate coverage to protect their property and financial well-being. Compliance with local regulations is not merely a bureaucratic hurdle; it's a cornerstone of proactive risk management and essential for maintaining the value of a property in flood-prone areas. This awareness is crucial in avoiding costly and time-consuming legal complications or potential financial losses due to insufficient coverage in a water backup event.

7. Financial Capacity

Financial capacity plays a critical role in determining the appropriate level of water backup coverage. Adequate insurance reflects an understanding of potential financial burdens associated with water damage. This consideration encompasses both the immediate costs of repair and the long-term implications for recovery.

- Asset Valuation and Loss Estimation

Accurate assessment of assets at risk, including the property itself and its contents, is essential. Evaluating the replacement value of the home, fixtures, and personal possessions provides a baseline for understanding potential losses. Comprehensive estimations of potential damage are crucial in calculating the necessary insurance coverage. A high-value property with expensive fixtures and extensive contents requires higher coverage compared to a property with lower value contents and simpler design. This careful assessment allows for the selection of a coverage level that aligns with the value of the assets at risk.

- Existing Financial Resources

Evaluating existing financial resources, such as savings, insurance policies, and available credit lines, is vital. This assessment helps ascertain the financial cushion available to absorb unexpected losses. Individuals with substantial savings and strong credit can afford higher coverage levels than those with limited resources. This contrasts with circumstances involving limited financial capacity, where selecting a lower coverage amount aligns with the available resources and ensures the option to address other financial obligations. The choice of coverage level must consider realistic financial possibilities for recovery.

- Future Financial Obligations

Considering future financial obligations, such as mortgages, student loans, or child support, is critical. These obligations impact the ability to absorb potential losses. A realistic assessment of ongoing financial responsibilities informs the coverage needed. This avoids overextending one's resources by selecting a policy limit that exceeds one's financial capability, leaving them inadequately prepared to handle the potential financial strain of an incident.

- Risk Tolerance and Budgetary Constraints

Individual risk tolerance and budgetary constraints influence the level of coverage selected. Individuals with a higher risk tolerance might opt for a broader range of coverage, while those with lower risk tolerance might prioritize minimizing premiums. This individual evaluation should consider long-term financial goals and personal circumstances, ensuring a comprehensive approach to protecting assets and financial stability.

Ultimately, aligning water backup coverage with financial capacity provides a comprehensive strategy for managing potential losses. By considering asset valuation, existing resources, future obligations, and individual risk tolerance, individuals can make informed decisions regarding the appropriate coverage amount. This ensures a protective measure that aligns with financial realities, mitigating the potential for devastating financial impact in the event of a water damage incident.

Frequently Asked Questions

This section addresses common inquiries regarding the appropriate level of water backup insurance. Clear answers to these questions aim to facilitate informed decision-making regarding adequate protection.

Question 1: How do I determine the value of my property for insurance purposes?

Property valuation for insurance purposes typically involves assessing the current market value of the structure and contents. This often entails professional appraisal services, which consider factors such as the property's age, condition, location, size, and features. Replacement cost, which reflects the current cost of rebuilding or replacing items, is frequently a crucial element. Comprehensive documentation of renovations, improvements, and existing contents is vital to accurately reflect the property's current value and establish a precise basis for insurance coverage.

Question 2: What factors influence the flood risk assessment for my area?

Flood risk assessment considers historical data, geographical location, and local regulations. Historical flood records, including the frequency and severity of past events, are crucial. Geographic factors such as elevation, proximity to water bodies, and soil composition influence flood risk. Local regulations and flood maps, often publicly available, delineate flood zones and provide detailed information about the potential for flooding in specific areas.

Question 3: How does contents coverage differ from structure coverage?

Structure coverage addresses damages to the physical building, while contents coverage pertains to personal belongings. The value of furniture, appliances, and other items must be meticulously assessed to determine appropriate contents coverage. Policies may vary in whether they offer replacement cost or actual cash value for damaged items. Understanding the specifics of these policy options is crucial in determining sufficient protection for both the structure and its contents.

Question 4: Are there specific items that need specialized coverage?

Certain items may necessitate specialized coverage due to their unique value or vulnerability to water damage. Valuables like jewelry, antiques, or artwork often require detailed appraisals to ensure sufficient coverage. Electronics and other potentially expensive items may also necessitate specific provisions. Detailed assessments by qualified appraisers for these high-value items are often required to secure accurate coverage.

Question 5: What is the significance of local regulations in determining water backup coverage?

Local regulations frequently mandate minimum insurance coverage levels, especially in flood-prone areas. Compliance with these ordinances is vital for maintaining property rights and avoiding potential penalties. Understanding these requirements provides a clear understanding of the level of coverage considered suitable and legally compliant in a particular location.

In summary, determining the right water backup coverage necessitates careful evaluation of property value, flood risk, coverage options, and financial capacity. Compliance with local regulations is also critical. Seeking professional guidance can help individuals navigate these complex factors to secure appropriate coverage and protect assets effectively.

This concludes the Frequently Asked Questions section. The subsequent section will delve deeper into practical steps for obtaining water backup insurance.

Conclusion

Determining the appropriate level of water backup coverage necessitates a multifaceted approach. The value of the property and its contents, coupled with the assessed flood risk, are primary considerations. Policy limits, encompassing structure, contents, and additional living expenses, must align with the potential financial burden of a water damage event. Understanding the available coverage options and adhering to local regulations are equally critical. Furthermore, financial capacity plays a vital role, as sufficient funds are required to absorb potential losses and facilitate recovery. An accurate assessment of these interconnected factorsproperty valuation, flood risk, policy limits, coverage options, local regulations, and financial capacityis essential for securing appropriate protection. Failure to account for any one of these elements can leave one vulnerable to significant financial hardship during a water backup event.

Ultimately, a thorough and informed understanding of water backup coverage is crucial for financial preparedness. Proactive assessment of potential risks, coupled with appropriate planning and financial strategies, mitigates potential losses. This meticulous process ensures that individuals and businesses are adequately protected against the considerable financial ramifications of water damage. Implementing these principles is essential for safeguarding assets and maintaining financial stability in the face of unexpected water backup events.

Mint Coldwater Michigan: Coolest Spots & Activities!

Home Depot Stock Price: Latest Updates & Analysis

David N Watson: Expert Insights & Strategies